Ulta Beauty is the largest specialty beauty retailer in the United States operating more than 1,350 stores across all 50 states. Specialty beauty retail is essentially stores that offer products such as make-up, skin care, fragrance and hair care where Ulta mainly competes with Sephora (owned by LVMH).

Historically, beauty products were primarily sold at large grocery retailers and department stores such as Macy’s. However, the industry has seen a channel shift over the past few decades with more of the sales coming from e-commerce and specialty beauty retailers – between 2015 and 2021, specialty beauty retail grew from 10% to 15% of channel distribution while grocery declined from 24% to 21% over the same frame. Ulta Beauty commanded ~9% share of the $104 billion beauty products industry in 2023, per the FY23 annual report. Despite Ulta owning a larger piece of the market compared to a decade ago, the industry remains fragmented.

Importantly, the beauty products market is also growing. At the time of Ulta Beauty’s first annual report as a public company in early 2008, the market was estimated to represent about $35 billion in retail sales. That means the addressable market has grown at ~7% CAGR over the past 15 years. Ulta also competes in the salon service industry with full-service hair salons available in most of its stores, but estimates that it has less than 1% share of that market. About 3% of Ulta’s revenue in FY22 came from the services category, which also includes skin and makeup services in select stores.

“Expand Market Leadership and Drive Profitable Growth”

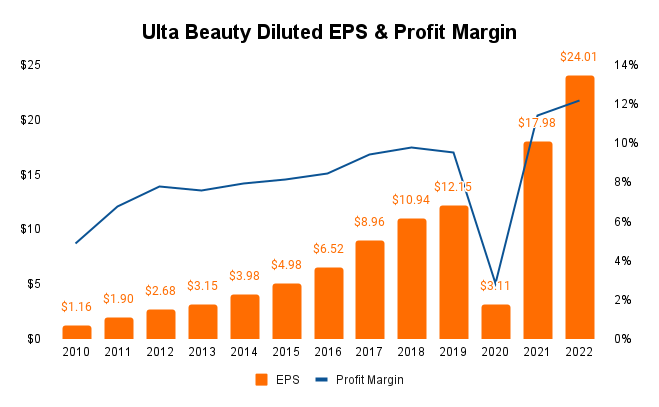

Between Ulta’s IPO in late 2007 and the end of FY22, Ulta Beauty shares compounded at ~17.8% annually. That includes a 85% drawdown during the heights of the financial crisis in 2008 (Ulta actually managed positive sales growth during all years of the GFC) and a 60% drawdown in March 2020. Diluted EPS has increased by more than 25% annually on average over the same time frame with profit margins expanding from 7% to 12% as of FY22.

One of the most impressive parts about this story is that a retailer like Ulta with no apparent pricing power and low switching costs has been steadily improving margins over the past decade. How? Part of the reason is that Ulta has gained access to more prestige brands as it has become a nationally recognized retailer. For example, prestige brand collection MAC Cosmetics started to sell its products in 25 Ulta Beauty stores as well on Ulta’s e-commerce platform to begin with back in 2017. Today, you can find MAC Cosmetics in nearly every Ulta location. The story is similar for brands like Clinique and Estèe Lauder as well.

Furthermore, the fact that Ulta Beauty stores carry mass-market, prestige and mass-tige brands means they appeal to a wide range of consumers. A typical Ulta store stocks more than 500 brands compared to a Sephora store which carries around 200 brands (per Morningstar), allowing consumers to choose from a larger assortment and across multiple price points. Getting more customers in the door is a good long-term strategy because many of these customers eventually will migrate towards more prestige brands at some point. That – of course – relies on Ulta’s ability to retain these customers, which is where the rewards program becomes important.

Ulta’s Rewards program (named Ultamate Rewards) is proof that Ulta has successfully managed to become a destination for both mass and prestige across beauty categories. Ultamate Rewards had 42.2 million active members at the end of the last quarter (Q3 2023), and a whopping 95% of total sales comes from rewards members. Further, the rewards program allows Ulta to convert customers that typically only buy in-store into multi-channel shoppers:

“Converting these members to omni-channel members is a meaningful opportunity to increase engagement and spend per member as omni-channel shoppers spend 2.5 times to 3 times more than single channel shoppers. Importantly, the increase in spend is largely incremental”

Ulta Beauty Collection, Ulta’s private label brands, has also likely contributed positively to margins over the past decade. Private label allows Ulta to deliver differentiated products and packaging that adds to its value proposition of having more products and brands compared to competitors. Even though Ulta does not break out private labels sales alone, private label and exclusive product penetration together has increased from 4% of sales in 2016 to 10% of total sales in fiscal 2022.

Capital allocation

At the 2018 Analyst Day, Ulta updated its store maturation target from 1,200 stores to a range of 1,500-1,700 (currently at 1,374 stores as of 3Q23). The store maturation target has increased over the years, all while actual new store openings have slowed down. Ulta has historically opened between 75 and 80 new stores per year but guided for 50 net new stores annually between 2022 and 2024 when management announced an updated long-term outlook back in 2021. Ulta opened 47 net new stores in FY22 and is guiding for 25-30 new stores in FY23.

Over the past decade, Ulta has spent a significant amount of capial on new store openings and relocations, as well as and remodeling, IT systems and supply chain. With less capex expected to be deployed for new store openings, capex as a % of sales will likely decrease in the years ahead – Ulta spent about 8% of sales on capital expenditures between FY12-FY18 while it is forecasting 4%-5% of total sales over the next few years.

Ulta does not pay dividends, but returns capital to shareholders through fairly substantial share repurchases. Since the number of diluted shares outstanding peaked at 64.7 million at the end of FY14, Ulta has repurchased close to 25% of its shares. That is equivalent to a ~3% annual decrease in shares outstanding. Ulta currently has $250 million available under the $2 billion share repurchase program that was announced in March 2022. With the current pace of buybacks ($281.5 million in 3Q23), it is reasonable to believe that a new repurchase program will be announced with the Q4 earnings numbers in early 2024.

With the change in expected capital allocation priorities and less capex spend relative to sales, Ulta’s historical returns on capital may not be a good guide of what it will look like over the next decade. Regardless, Ulta has generated 25-30% return on capital in most years with a very conservative balance sheet which includes no long-term debt. Ulta’s main capital priority is to reinvest in its business before returning excess capital to shareholders (per the 2021 Analyst Day), which management has done successfully for many years.

Less capital deployed towards new stores will give Ulta more optionality going forward. In August 2021, Ulta announced a partnership with Target (“Ulta Beauty at Target”) that includes 1,000 square feet of dedicated space designed to mirror the Ulta Beauty experience within Target stores. In the most recent quarter, Ulta opened 89 Ulta Beauty at Target shops and now operates a total of 510 shops in Target stores around the country. Ulta management expects that number to ramp up to 800 shops over time, and given the speed of new Ulta Beauty at Target openings that will be sooner rather than later. It is reasonable to think that Ulta will have an update for investors within 1-2 quarters on what Ulta Beauty at Target shop openings will look like going forward.

Ulta does not break out sales from Ulta Beauty at Target alone but incorporates it in the “Accessories & Other” segment that accounted for 3% of revenue in FY22. Management does not provide much context on the growth or specific numbers related to Ulta Beauty at Target, but CFO Scott Settersten said on the most recent earnings call that “gross margin pressures were partially offset by strong growth in other revenue, primarily due to growth in both credit card income and royalty income from our Target partnership.” That should make shareholders confident that the Ulta Beauty at Target initiative is paying dividends already.

On the topic of optionality, there is an added level of uncertainty compared to what it has been like since Ulta initiated its high growth face in the 2000s and 2010s. A decade ago it was obvious that the path forward would include a whole lot of new stores and that the majority of capital expenditures would go towards new stores. As Ulta gets closer to store maturity, the road ahead is not as straightforward. The question is what the next step will be, whether that is expansion beyond U.S. borders or if there is a different trick up management’s sleeve. With the success of Ulta Beauty at Target so far, I think management has shown that they have the ability to find attractive capital allocation opportunities. It is too early to conclude, of course.

Valuation

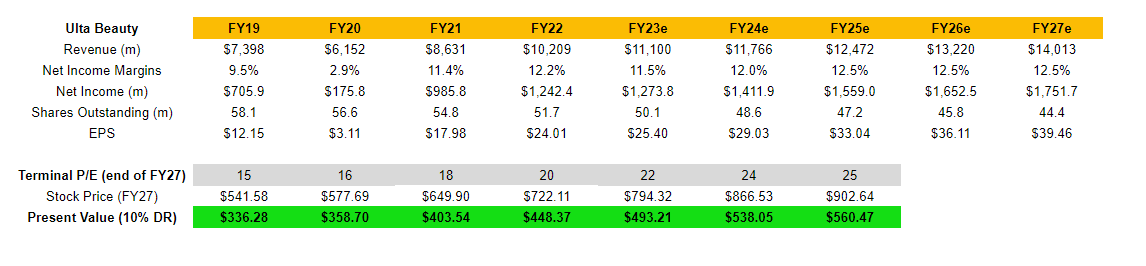

Below is my current earnings model for Ulta. The key assumptions are as follows:

- Ulta will hit the midpoint of the guidance for FY23 which includes net sales in the $11.1B to $11.15B range and EPS between $25.2 and $25.6

- 6% annual revenue growth between FY24 and FY27

- Profit margins will stabilize at 12.5% and a 3% annual reduction in shares outstanding will lead to EPS growing between 9-10%

Considering that Ulta is expecting low double digit EPS growth, these are fairly conservative assumptions. There is also a good chance that we will see further margin expansion, whether that be from some of the current investments in supply chain efficiencies or e-commerce. Management has clearly demonstrated an ability to increase margins over the past decade, and I think it would be reasonable to assume 13-14% profit margins in one were to look at a bull case.

The current valuation of ~19x FY23 earnings (share price of $480 and $25.4 in EPS) looks pretty attractive. Only a few months ago Ulta was trading below $400 as Mr. Market was concerned about declining operating margins, higher shrink and more cautious consumers; these concerns were partially addressed at the most recent earnings call as management called out that “the beauty category remains healthy and consumer engagement remains high.” However, the CFO also emphasized that “2023 is an extraordinary investment year”, and that a lot of the investment is coming through the SG&A line which impacts the operating and net income margins. If successful, these investments will have a short-term negative impact on margins but lead to top line growth and margin expansion in the long run.

The question that remains is what a fair multiple for Ulta Beauty looks like. Among the reasons why Ulta should trade at an above average multiple is the loyal customer base, tailwinds from a growing beauty industry and the opportunity to upsell new and existing customers (from mass-market to prestige brands and single channel to omni-channel shopping). Moreover, the fact that Ulta has cash on hand and no long-term debt also provides more optionality going forward, whether that is further investments into cost saving initiatives, digital or expansion into Canada/Mexico down the line.

However, retailers operate in a highly competitive environment with low switching costs and low margins under constant pressure to strike the right balance when it comes to inventory management and investments. My take is that a specialty retailer like Ulta likely deserves a multiple slightly higher than where it trades today, but also that the next decade will look different from the past decade (slower growth and fewer new stores). That leaves room for interpretation whether the current multiple is too low or if the market is correct in assigning a <20x earnings multiple to Ulta Beauty.

Ulta Beauty checks off many of my boxes. However, I am still not sure how I want to play the growing beauty industry. There are benefits to owning a brand owner (e.g. L’Oréal), but the retail side remains fragmented and Ulta is in a good position to continue to take market share. As a retailer, Ulta can also quickly adopt to changes in demand from emerging brands. That seems to be important with the impact of social media and influencers trying to disrupt legacy brands. It is arguably easier to create a beauty brand today than it was only a few decades ago. I do not own shares of Ulta Beauty as of today, but continue to follow the company closely while I organize my thoughts on the industry.

Disclaimer: This is not a recommendation to buy or sell stocks. Top Corner Investing is for informational purposes only, I am not a professional and I do not provide financial advice. Please do not buy or sell stocks without doing your own research and/or consulting with a professional.

Leave a comment